Health insurance was built on the premise that profit could be made by pooling the monthly premiums of a large group of people attempting to finance their medical costs and balancing the risk of medical claims against those paid premiums. While that makes sense to the insurance companies, what if things could be done better?

The pioneers of health care sharing asked themselves how they could design a better system when they decided to revolutionize the world of healthcare financing. What emerged was the non-profit health care sharing organization: a system free of profit motives, free of the lack of transparency, and free of the cold, impersonal treatment that health insurance companies force customers to accept.

Health Care Sharing Works Better

Health insurance is fundamentally a financial transaction. Health insurance companies charge a premium as payment for putting their capital at risk in the form of promises to pay consumer medical expenses. Therefore, health insurance companies view medical bills as a business expense and seek to minimize those bills, often at the expense of policyholders’ overall health.

Health care sharing, on the other hand, is a system that is significantly more efficient, based on shared risk and responsibility. It offers more choice and is significantly less expensive than health insurance. Health insurance companies exist to generate profits and have every motivation to push premiums and deductibles as high as possible. Health care sharing organizations are non-profit organizations that exist solely to benefit their members and to pay their member’s medical bills.

A health care sharing organization brings together the financial resources of its members, in the form of monthly member contributions, to achieve an ability to fund medical bills comparable to that of insurance. This approach differs from health insurance, however, in that it applies all of the financial power of those funds to pay medical bills with none set aside for profits.

Government rules and regulations have done nothing to health insurance companies but unwittingly incentivize them to push deductibles and premiums higher. Health care sharing is able to keep monthly contributions and personal responsibility for medical bills low by being solely organized for the purpose of keeping costs down.

Health Care Sharing Feels Better

Nothing about interacting with insurance companies as a policyholder feels right these days. The system is broken. The Affordable Care Act (ACA) has not delivered promised efficiencies and lowered out-of-pocket expenses. The ACA has only exacerbated the dysfunction of state health insurance markets.

Health care sharing organizations are built on a foundation of shared humanity, the natural human instinct to support and encourage others that is the lifeblood of a community. This foundation allows for a better system that evokes more confidence in its members — confidence that their medical bills will be paid and their financial contributions to the organization will go to paying the medical bills of their peers.

A health care sharing organization always operates in the best interest of its members, for whom out-of-pocket expenses are kept low. Members also enjoy the benefit of knowing how much their care will cost in advance, thanks to published rates. This visibility and affordability results in increased disposable income for health care sharing members. This allows members to concentrate on family activities, college funds, or saving up for a home, without sacrificing the quality of care their family receives.

A health care sharing organization is focused on taking care of its members because its members are focused on taking care of each other.

Shared Humanity and Responsibility Replaces Corporate Finance

Health insurance companies are businesses. Their primary purpose is to ensure a return on the financial assets that they possess. When they write health insurance policies, they do so for the sole purpose of realizing a return.

Health insurance is highly regulated by state boards of insurance, to ensure that they retain enough financial resources to support the policies that they write. Health insurance is further regulated by the federal government through the ACA provisions, including those related to medical loss ratio. A medical loss ratio is, simply put, the ratio between claims paid and premiums collected. The ACA rules require that health insurers spend at least 80% of premiums collected on claims paid. In other words, the ACA attempts to legislate that health insurance be required to limit their profits and use the majority of premiums to pay policyholder’s medical bills.

However, the medical loss ratio component of the ACA has had a huge unintended consequence. By attempting to control the profit of health insurance companies, the ACA has actually caused inflation in premiums and total health care out-of-pocket expenses. The ACA has driven health insurance companies to raise premiums and deductibles in an attempt to increase the size of the 20% of premiums that the medical loss ratio allows to go toward their profits.

There is just no getting around the fact that health insurance in the US is a structurally flawed system, assuming that the goal is to reduce the overall cost of health care and ensuring that medical bills do not have a materially negative impact on the finances of the people who depend on it.

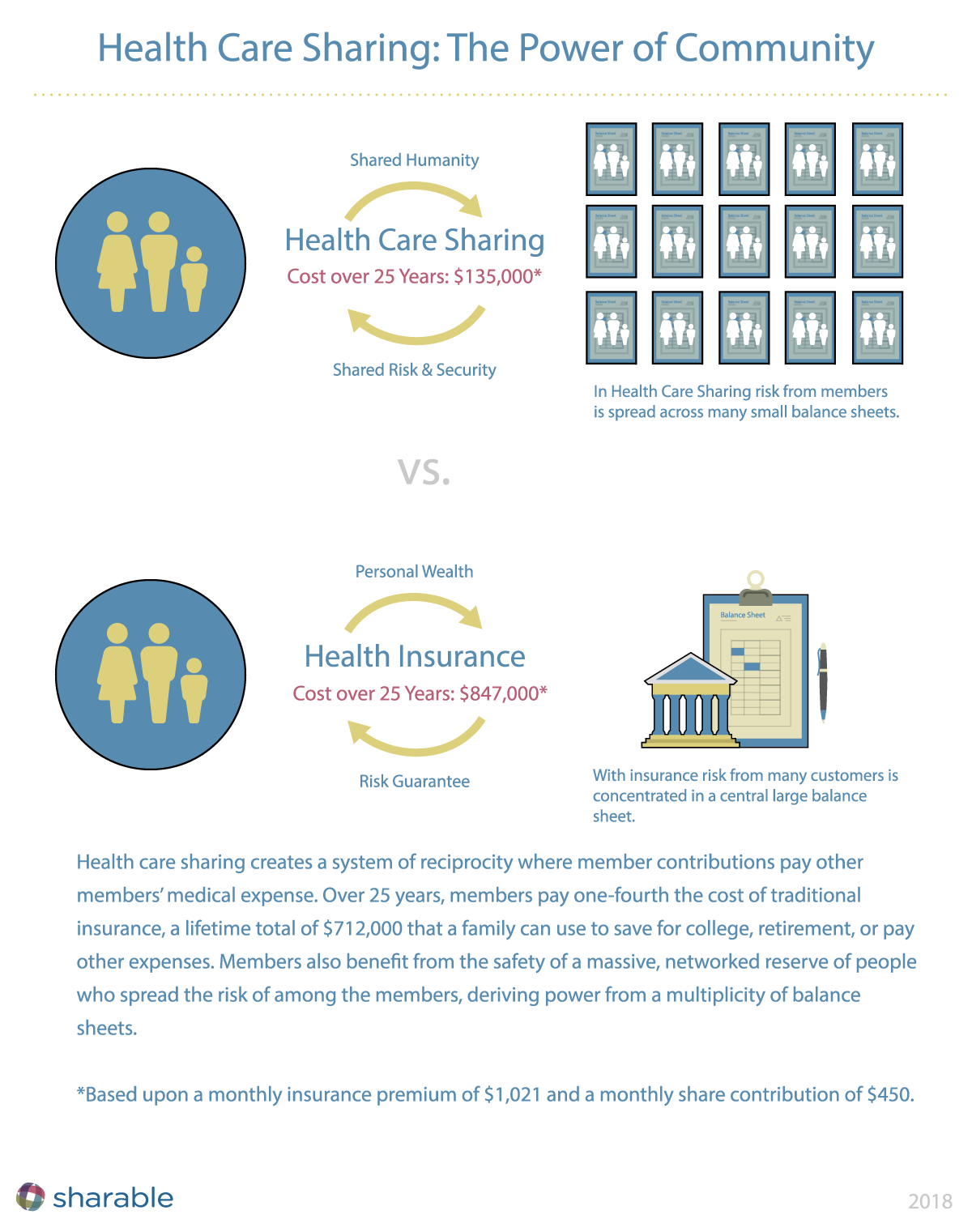

Health care sharing comes at the problem from a completely different angle, utilizing the non-profit model — in the form of a health care sharing organization — to organize the participation of large numbers of individuals with a common set of values and goals. Ultimately, those values revolve around shared humanity, shared risk, and shared financial responsibility for helping others live healthy lives. The sole purpose of a health care sharing organization is to pay the medical bills of its members. It does so by combining the small monthly deposits of a large number of members into a P2P network of shared accounts that is comparable to the large balance sheets of the health insurance companies. A very large number of small balance sheets forms a stronger network than a single large balance sheet of an insurance company where there is one point of failure.

To demonstrate the profound difference in the performance of these two health care expense funding structures, let’s look at a specific scenario — the lifetime financial impact of for a family of three.

The monthly share contribution paid by members of a health care sharing organization, in this case, a family of three, would amount to a total cost of $135,000 over 25 years.

For a family of the same size with health insurance, however, the premiums paid would amount to $306,000 over 25 years, which is $171,000 more than health care sharing. Taking into account the lost investment opportunity at a rate of 6% return per year, health insurance would cost this family $847,000 over 25 years.

The members of the health care sharing organization would pay just 15% of the cost of an equivalent health insurance policy. That is a staggering difference of $712,000, more than enough to fund an excellent education for their child, ensure that they own their family home, and offer a great start on their retirement savings.

The promise of health care sharing is this: by organizing the shared humanity of like-minded members to work together and share the risk of paying medical bills, funds equivalent to the profits of a health insurance company can instead stay in the hands of the members, having a significant impact on the quality of their lives.

Health Care Sharing Organizations Exist to Pay Medical Bills

Health care sharing is founded on the idea of community and shared humanity. But what exactly is shared humanity? Humanity is an intangible concept, but its effect on our society is certainly easy to observe. It is everything from the high school kids who shovel the snow from the widow’s driveway, to the thousands of volunteers who build homes for Habitat for Humanity, to the hundreds of thousands of dollars that are donated to the GoFundMe page posted on behalf of a family that has experienced a disaster or tragedy.

Health care sharing organizations institutionalize shared humanity. The first component of shared humanity is motive. Like the selflessness demonstrated in the examples above, a health care sharing organization exists to serve its members. There are no financiers, shareholders or other financial stakeholders to consider. There is no opposition or disincentive to paying the needs and expenses of the members. Instead there is shared responsibility for seeking options and making informed choices. The contrast between health care sharing organizations and health insurance corporations could not be more stark in this respect. The need for financial return that is implicit in a health insurance policy is completely absent from health care sharing. As a result, members can be confident that their needs will be met, both in terms of the health care they need and payment for that care.

The second component of shared humanity in a health care sharing organization is transparency. The role of the health care sharing organization is to bring providers, labs, pharmacies and imaging resources to the table on behalf of the members. This is done in a way that allows members to understand and weigh options in a manner never before experienced in health care. In the most innovative health care sharing organizations, each member with a need has access to a highly-trained patient advocate whose sole mission is to identify health care options and explain them in terms that can be easily understood. A major component of this is fully understanding the cost of a course of action before it is embarked upon.

Health insurance works with providers in way that could be described as opaque at best. Health insurance policyholders are dependent on the very providers that they are paying to guide them through their options in the time of medical need. It is often difficult to differentiate between options that the provider offers and those that are most effective. Often a “second opinion” directly contradicts the opinion of the first provider. To make that even worse, policyholders have no idea what expenses are being incurred until they receive an explanation of benefits (EOB) months after care is provided. A major component of the EOB is a set of citations of the policy describing why an expense is not covered, or is not fully covered, by the policy. It can all be a frightening and disheartening experience.

The final component of shared humanity in a health care sharing organization is mutual support, which takes multiple forms. Medical bills submitted to a health care sharing organization are matched to members who have deposited their monthly contribution into their share accounts. Those contributions are then used to share in the payment of medical bills. Members are then able to see, not only the members who receive their money each month, but also which members share in their medical bill, if and when they have a medical event. This level of transparency and visibility connects everyone to the way their monthly contributions are being used: to help others.

Additionally, members have the option to offer more than just the funds needed to pay a medical bill. In these times of need, a human touch is invaluable. Health care sharing organizations offer members the opportunity to exchange words of support and encouragement or prayers on behalf of their peers. This form of social interaction is uplifting and edifying for both the giver and the recipient.

Health Care Sharing Organizations Bring Health Care Options to Members

In the run-up to passage of the ACA, President Obama made a now infamous pledge that under the new law, “patients would be able to keep their doctor.” Now, a few years into implementation of the ACA, the facts contradict this pledge. Both insurers and providers are looking for ways to exist within the labyrinth of government rules and regulations that has become the US healthcare system.

One of the favorite new models for highly regarded medical providers these days is referred to as concierge medicine. In this model, highly capable providers charge annual subscription fees to patients that can afford to buy their services, thus creating a system of haves and have-nots in medicine. This is yet another unintended side effect of the ACA, limitation of access to health care by creating a dual-tier system.

The net result of ACA regulation is that even the number of health insurance providers operating within ACA is diminishing significantly over time.

Health care sharing is not subject to the regulations associated with the ACA, in particular, the minimum essential benefits rules. The minimum essential benefits rules require that every health insurance policy covers ten specific benefits, even if the policyholder in question has no use for them. Consider younger childless men: under ACA, his policy would include numerous pediatric services, even though he has no children. This is unfortunate in that it drives a significant increase in premium by including services that are of no use to the policyholder. In addition to driving up cost with unnecessary services the ACA’s mandated benefits require Americans to pay for services that some find objectionable, based on matters of faith and religion.

Health care sharing organizations seek to align the capabilities of their organization with the needs and expectations of their members. Some health care sharing organizations have begun to aggregate hundreds of thousands of physicians, providers, medical support services, imaging and diagnostic centers, pharmacies and other services, such as telemedicine providers, as part of their health care options. In fact, some health care sharing organizations are integrating mechanisms that enable members to invite their favorite providers into the health care sharing network, for their own access and for that of other members.

Furthermore, part of this process is the negotiation of preferred rates, based upon the collective purchasing power of their members as a whole. The rates that are negotiated by the organization are then published for members to use, along with their patient advocate, to make informed decisions about which course of action is best for their situation, taking need, risks and costs into consideration. In this way, providers openly compete for the ability to provide care based upon metrics that include cost of care as well as quality of care.

Health Care Sharing Eliminates Structures That Increase Cost of Care

Although well intentioned, US health care reform in the form of the ACA has resulted in a foundational structure that has only increased the cost of health care in the US.

It has done so via a number of mechanisms, including:

- Minimum essential benefit rules in the ACA, which require that every policy contain coverage for a package of services deemed essential by the government. This has resulted in increased premiums, increased deductibles and increased out-of-pocket expenses.

- Medical loss ratio rules that limit the profits of health insurance policies to less than 20% of premiums. Health insurance companies are motivated by this system to raise premiums.

- A reduced number, due to ACA regulations, of both providers offering care through health insurance and companies offering health insurance. This reduction of competition has resulted in increased charges by health care providers that has in turn resulted in increases in premiums, deductibles and maximum out-of-pocket thresholds.

Health care sharing organizations exist solely to pay medical bills for members. They are non-profits with no profit motivation whatsoever. Therefore they can replace profit with lower contributions and personal responsibilities for their members.

Health care sharing organizations seek to expand access to care by striking agreements with as many providers as possible. Providers that works within the most innovative health care sharing organizations are invited and empowered to publish rate for all of their members to see, thereby encouraging competition and creating an environment in which members receive the best quality of care at the lowest cost of care.

Health care sharing organization members pay a monthly member contribution (typically an amount ranging from $45-$627 for individuals). In 2017, Americans spent an average of $393/month for individual insurance coverage, or $1,021/month for family insurance coverage. In comparison, the typical health care sharing organization member paid approximately $450/month for a family.

Health Care Sharing Replaces Corporate Profit With Personal Wealth

While premiums, deductibles and total out-of-pocket have been rising under ACA, it does not seem to have had a negative effect on the profitability of most of the major health insurers.

The table below demonstrates that health insurance companies are actually thriving. The tradeoff between corporate profits and access to care/cost of care does not seem to be happening as the framers of the ACA intended.

Health care sharing organizations are non-profits. They exist solely to pay the bills of their members. They work to provide excellent access to care while keeping the cost of care, in the form of expenses related to each procedure or service, monthly member contribution, annual member responsibility, and out-of-pocket expense to a minimum.

As a result, these savings contribute to the personal wealth of members, not to the corporate profit of health insurance companies.

Health Care Sharing Works Better & Feels Better

The health care sharing model creates a reality in which Americans no longer need an insurance middleman to mitigate the risk and costs of a catastrophic health event. Although each organization operates slightly differently, they are all founded on the principle of collective moral responsibility and shared humanity. This is in stark contrast to the for-profit health insurance model to which we are all accustomed.

Warren Buffett said recently, when discussing the problems with American healthcare, that “hard as it might be, reducing healthcare’s burden on the economy while improving outcomes for employees and their families would be worth the effort. Success is going to require talented experts, a beginner’s mind, and a long-term orientation.” Health care sharing organizations share the belief that a community acting for and among itself can successfully defend its members against that rise in cost, ensuring patient engagement and positive health outcomes.

Underlying all health care sharing organizations is the belief that a community driven to achieve the best care at the lowest price can do so. By leveraging our natural desire to support and care for our fellow human beings, health care sharing can solve the complex issues surrounding affordable healthcare in America. Health care sharing organizations are ultimately based upon the fundamental principles of compassion, accountability, and transparency. It’s time insurance companies took notice that applying these concepts to healthcare not only works better, it feels better.